Gaming Industry Revenue Statistics 2026

wp:html

html

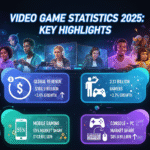

The gaming industry revenue statistics for 2026 paint a picture of unprecedented growth and transformation. With the global market reaching $522.5 billion, the sector continues to shatter records across every metric imaginable. Mobile gaming leads the charge while new technologies reshape how billions of players worldwide engage with interactive entertainment.

Understanding these gaming industry revenue statistics becomes crucial for developers, investors, and analysts navigating this dynamic landscape. From the explosive growth in cloud gaming to the maturation of esports ecosystems, every segment presents unique opportunities and challenges that define the modern gaming economy.

Gaming Industry Revenue by Platform Statistics 2026

Platform diversification remains central to the gaming industry revenue statistics narrative in 2026. Mobile gaming maintains its position as the dominant force, generating $196.8 billion and commanding 37.7% of the global market share. This represents substantial growth from the $92.6 billion reported in 2024, demonstrating mobile’s unstoppable momentum.

Console gaming holds steady at $123.5 billion, capturing 23.6% of the market despite facing increased competition from other platforms. PC gaming generates $98.2 billion, representing 18.8% of total revenue, with growth driven by digital distribution platforms and the expanding catalog of titles optimized for personal computers.

Cloud gaming emerges as the fastest-growing segment, reaching $54 billion with a remarkable 10.4% market share. This represents explosive growth from just $8 billion projected earlier, as improved infrastructure and 5G rollouts enable seamless streaming experiences. VR/AR gaming contributes $50 billion, accounting for 9.5% of the market, driven by Meta Quest 3 and Apple Vision Pro adoption.

| Platform | Revenue (USD Billions) | Market Share (%) | YoY Growth (%) |

|---|---|---|---|

| Mobile Gaming | $196.8 | 37.7% | 22% |

| Console Gaming | $123.5 | 23.6% | -1% |

| PC Gaming | $98.2 | 18.8% | 4% |

| Cloud Gaming | $54.0 | 10.4% | 22% |

| VR/AR Gaming | $50.0 | 9.5% | 15% |

Regional Gaming Industry Revenue Distribution 2026

Geographic analysis of gaming industry revenue statistics reveals Asia-Pacific’s continued dominance with $210.3 billion in revenue, experiencing 14.2% year-over-year growth. China alone contributes $105.9 billion, while Japan adds another $20 billion to the regional total. The mobile-first gaming culture in these markets drives consistent expansion.

North America generates $142.7 billion with an 11.8% growth rate, benefiting from high average revenue per user and mature monetization strategies. The United States accounts for $47 billion of this total, supported by strong console and PC gaming traditions alongside growing mobile adoption.

Europe contributes $98.6 billion to global gaming revenue, posting 9.5% growth despite economic headwinds. Germany and the United Kingdom lead the region in both console sales and PC gaming engagement. Latin America shows impressive momentum with $42.4 billion in revenue and 13.1% growth, while Middle East & Africa reaches $28.5 billion with the highest growth rate at 15.6%.

For those looking to explore popular gaming titles, the regional preferences vary significantly, with mobile dominating in Asia while consoles remain strong in Western markets.

Gaming Industry Revenue Growth Projections

Market analysts project continued expansion through 2030, with various research firms estimating global revenue between $600 billion and $691.3 billion depending on market definition scope. The compound annual growth rate from 2026 to 2030 is expected to maintain between 10.37% and 13.20%, driven by emerging technologies and expanding user bases.

Mobile gaming will likely maintain its position as the largest segment, though growth rates may moderate as the market matures. Console gaming faces potential resurgence in 2026 and 2026 with anticipated major releases including Grand Theft Auto VI and other tentpole franchises that could reinvigorate the segment.

Top Gaming Companies Revenue Statistics 2026

Corporate performance within gaming industry revenue statistics showcases Tencent Games maintaining global leadership with $38.9 billion in revenue, primarily from mobile and PC segments. Honor of Kings and PUBG Mobile continue driving the company’s mobile dominance across international markets.

Sony Interactive follows with $32.4 billion, boosted by PlayStation Plus subscriptions and exclusive titles. Microsoft Gaming generates $30.1 billion, benefiting from Game Pass growth and the Activision Blizzard acquisition. NetEase contributes $19.7 billion through mobile and MMO titles, while Nintendo adds $18.2 billion from console and handheld gaming.

| Company | 2026 Revenue (USD Billions) | Primary Segment | Key Franchises |

|---|---|---|---|

| Tencent Games | $38.9 | Mobile & PC | Honor of Kings, PUBG Mobile |

| Sony Interactive | $32.4 | Console & Cloud | PlayStation, Spider-Man |

| Microsoft Gaming | $30.1 | Console & Cloud | Xbox, Game Pass |

| NetEase | $19.7 | Mobile & MMO | Fantasy Westward Journey |

| Nintendo | $18.2 | Console & Handheld | Mario, Zelda, Pokemon |

| Activision Blizzard | $15.6 | PC & Console | Call of Duty, Warcraft |

Gaming Demographics and Usage Statistics 2026

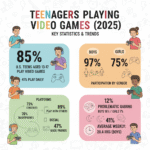

Demographic analysis within gaming industry revenue statistics reveals remarkable engagement across all age groups. Gen Z males lead with 91% participation rates, predominantly favoring mobile and console platforms. Millennials follow at 84% engagement, showing strong preferences for mobile and PC gaming experiences.

Gen Alpha emerges as a significant force with 78% gaming participation, rapidly adopting AR/VR platforms for educational and interactive experiences. Gen X maintains 62% engagement primarily through console and PC gaming, while Boomers show 39% participation, predominantly in casual mobile games.

Gender distribution approaches parity with women representing 48% of total gamers in the United States during 2026. This shift from previous years demonstrates gaming’s evolution into truly mainstream entertainment transcending traditional demographic boundaries.

Developers seeking to understand game development trends and insights must consider these demographic shifts when creating content for diverse audiences.

Player Engagement Metrics

Average revenue per user (ARPU) reaches $60.58 globally in 2026, though significant regional variations exist. North American players generate substantially higher ARPU due to greater purchasing power and willingness to spend on premium content and in-app purchases.

User penetration stands at 33.6% of the global population in 2026, projected to reach 37.4% by 2030. This represents approximately 3.42 billion active gamers worldwide, with Asia-Pacific accounting for 1.809 billion or 53% of the total player base.

Monetization Models in Gaming Industry Revenue 2026

In-app purchases dominate monetization strategies, contributing 41% of total gaming industry revenue. Titles like Genshin Impact and Roblox exemplify successful implementation of this model, generating billions through cosmetic items, character upgrades, and premium currency systems.

Subscription models account for 28% of revenue, with services like Xbox Game Pass and PlayStation Plus offering bundled access to extensive game libraries. This approach provides predictable revenue streams while reducing barriers to entry for players exploring new titles.

| Monetization Model | Revenue Contribution (%) | Key Examples | Growth Trend |

|---|---|---|---|

| In-App Purchases | 41% | Genshin Impact, Roblox | Stable |

| Subscription Models | 28% | Xbox Game Pass, PS Plus | Growing |

| Premium Games | 17% | Elden Ring, Baldur’s Gate 3 | Declining |

| Ads in Free Games | 9% | Hyper-casual mobile games | Stable |

| NFTs & Web3 Gaming | 5% | Axie Infinity, Illuvium | Emerging |

Premium game sales represent 17% of revenue, with titles like Elden Ring and Baldur’s Gate 3 demonstrating continued viability for high-quality, full-price releases. Advertisement-supported free games contribute 9%, particularly in the hyper-casual mobile segment where quick sessions and high player turnover maximize ad impressions.

Web3 gaming incorporating NFTs and blockchain technology captures 5% of the market. While still niche, this segment attracts crypto-savvy users interested in true digital ownership and play-to-earn mechanics, suggesting potential for future growth as technology matures.

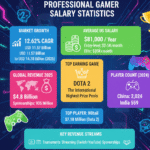

Esports Revenue Statistics 2026

Esports revenue within gaming industry statistics reaches approximately $3.25 billion in 2026, demonstrating robust growth from $2.73 billion in 2024. Sponsorships remain the primary revenue driver, contributing $935 million or roughly 29% of total esports revenue, with brands like Red Bull, Intel, and Logitech maintaining significant presence.

Media rights generate $450-600 million, representing 15-20% of esports revenue as streaming platforms and traditional broadcasters compete for exclusive content. The segment experiences rapid growth as established franchises with proven audience engagement command premium valuations.

Merchandise and ticketing each contribute 5-10% of esports revenue, totaling $150-300 million combined. Team-branded apparel, collectibles, and live event attendance benefit from increasing fan loyalty and improved distribution channels. Publisher fees add another $90 million through licensing agreements and official tournament organization.

Regional distribution shows North America contributing over $600 million to global esports revenue, while China adds approximately $445 million. The Asia-Pacific region maintains 57% of global esports viewership, cementing its position as the largest regional market for competitive gaming.

Esports Audience Growth

The global esports audience reaches 640.8 million users by end of 2026, nearly doubling from 2020 levels. This includes both dedicated enthusiasts and occasional viewers across major competitive gaming titles and tournaments. Women now represent 28% of the North American esports viewing audience, up from 22% in 2020.

Collegiate esports programs expand rapidly with over 240 U.S. colleges offering varsity programs with scholarships, compared to 175 in 2023. This institutional support legitimizes competitive gaming as a career path while developing talent pipelines for professional leagues.

Gaming Industry Development Trends 2026

Technological innovation drives gaming industry revenue statistics forward in 2026. AI-driven game design achieves 68% adoption rate, revolutionizing procedural content generation and NPC behavior. This technology reduces development costs while enhancing player immersion through dynamic, responsive game worlds.

Cross-platform play becomes standard with 61% implementation across major titles. Games like Fortnite and Call of Duty demonstrate seamless gaming across devices, breaking down traditional platform barriers and expanding potential player bases for developers.

Cloud streaming reaches 58% adoption, enabling no-download gameplay that removes hardware limitations. Services like Xbox Cloud Gaming report over 10 million active streamers, while NVIDIA GeForce Now reaches 25 million registered users, indicating strong consumer acceptance of streaming technology.

| Development Trend | Adoption Rate (%) | Impact on Industry |

|---|---|---|

| AI-Driven Game Design | 68% | Reduced costs, enhanced immersion |

| Cross-Platform Play | 61% | Expanded player bases |

| Cloud Streaming | 58% | Removed hardware barriers |

| Blockchain Integration | 42% | Digital ownership, NFT trading |

| Accessibility Features | 36% | Inclusive gaming for all users |

Blockchain integration expands beyond NFTs with 42% adoption, incorporating secure identity systems and asset tracking. While controversial, this technology addresses longstanding issues around digital ownership and cross-game asset portability.

Accessibility features reach 36% implementation, reflecting industry commitment to inclusive design. Developers increasingly recognize the importance of accommodating players with disabilities, expanding potential audiences while improving overall user experience.

Mobile Gaming Revenue Statistics by Country

Country-specific analysis of gaming industry revenue statistics highlights significant regional variations. The United States leads with $25 billion in mobile gaming revenue, followed closely by China at $40 billion despite regulatory challenges. Japan maintains third position with $18 billion, demonstrating strong per-capita spending.

South Korea, Germany, and the United Kingdom represent additional major markets, each showing steady growth particularly in esports, puzzle, and simulation genres. Emerging markets including India, Brazil, and Southeast Asian countries demonstrate rapid expansion driven by smartphone penetration and affordable data plans.

Online games dominate mobile revenue, capturing 65% of the segment through titles like Genshin Impact, PUBG Mobile, and Clash Royale. These games thrive on real-time multiplayer experiences and social features that drive engagement and monetization.

Offline games maintain relevance with 12% of mobile revenue, particularly in regions with inconsistent connectivity. India, Brazil, and parts of Southeast Asia show strong demand for games playable without constant internet access.

Industry Challenges and Market Dynamics

Despite impressive gaming industry revenue statistics, the sector faces significant challenges. Privacy regulations and platform policy changes, particularly Apple’s App Tracking Transparency framework, force developers to adapt monetization and user acquisition strategies.

Market consolidation continues with major acquisitions reshaping competitive dynamics. Microsoft’s Activision Blizzard acquisition and similar deals concentrate power among fewer companies, potentially impacting innovation and market diversity.

Rising development costs pressure studios to deliver increasingly sophisticated experiences while maintaining profitability. AAA game budgets now routinely exceed $100 million, creating higher stakes for publishers and potentially limiting creative risk-taking.

The shift toward live-service models transforms traditional development cycles. Games increasingly launch as platforms for ongoing content delivery rather than complete products, requiring sustained investment and community management.

Future Market Opportunities

Emerging technologies present substantial growth opportunities within gaming industry revenue statistics. Virtual reality approaches mainstream adoption as hardware costs decrease and content libraries expand. Apple Vision Pro and Meta Quest 3 lead consumer-friendly offerings that could catalyze mass market acceptance.

Artificial intelligence integration extends beyond development tools to gameplay experiences. Generative AI enables dynamic storytelling, personalized content, and responsive game worlds that adapt to individual player preferences and behaviors.

Cloud gaming infrastructure improvements through 5G deployment and edge computing reduce latency concerns that previously limited adoption. As technology matures, streaming could fundamentally reshape distribution models and hardware requirements.

The metaverse concept, while currently overhyped, represents long-term potential for interconnected gaming experiences. Successful implementation could create new revenue streams through virtual goods, services, and experiences transcending individual game boundaries.

FAQs

What is the total gaming industry revenue in 2026?

The global gaming industry generates $522.5 billion in 2026, growing from $475.2 billion in 2024 with a 10.2% compound annual growth rate.

Which gaming platform generates the most revenue?

Mobile gaming leads with $196.8 billion (37.7% market share), followed by console gaming at $123.5 billion and PC gaming at $98.2 billion.

How much revenue does esports generate in 2026?

Esports generates approximately $3.25 billion globally in 2026, with sponsorships contributing $935 million and media rights adding $450-600 million to total revenue.

What percentage of gaming revenue comes from in-app purchases?

In-app purchases account for 41% of total gaming revenue, making it the dominant monetization model ahead of subscriptions at 28% and premium games at 17%.

Which region has the highest gaming revenue growth rate?

Middle East & Africa shows the highest growth at 15.6%, followed by Asia-Pacific at 14.2% and Latin America at 13.1% year-over-year.

Sources:

1. Gaming Industry Report 2026: Market Size & Trends. Udonis Blog. Retrieved from https://www.blog.udonis.co/mobile-marketing/mobile-games/gaming-industry

2. Games – Worldwide Market Forecast. Statista. Retrieved from https://www.statista.com/outlook/dmo/digital-media/video-games/worldwide

3. Global Esports Revenue Statistics 2026. Coop Board Games. Retrieved from https://coopboardgames.com/statistics/global-esports-revenue-projections/

4. Gaming Market Size, Industry Share, Growth Report 2033. IMARC Group. Retrieved from https://www.imarcgroup.com/gaming-market

/wp:html